How to Use Blockchain for the Insurance Industry?

The application of blockchain solutions for insurance stands to bring massive benefits to the industry. In this article, we will discuss in detail the use of blockchain for the insurance industry. Let's start.

In this article

- Blockchain and Insurance

- Blockchain Use Cases for the Insurance Industry

- Blockchain Insurance App Development

- The Future: An Insurance Industry Powered with Blockchain

- Frequently Asked Questions on Blockchain for Insurance Industry

Blockchain and Insurance

Blockchain technology is being heralded by some as the catalyst for the 4th industrial revolution. Many claim that it will become the biggest disruptor of established industries like insurance.

Although the technology is still in its infancy, it promises to save businesses huge amounts of money by providing increased data security and streamlining paperwork and procedures.

With the advent of blockchain technology, insurance has found itself a powerful tool that has the power to transform many of the core processes the sector has come to rely on.

Get a complimentary discovery call and a free ballpark estimate for your project

Trusted by 100x of startups and companies like

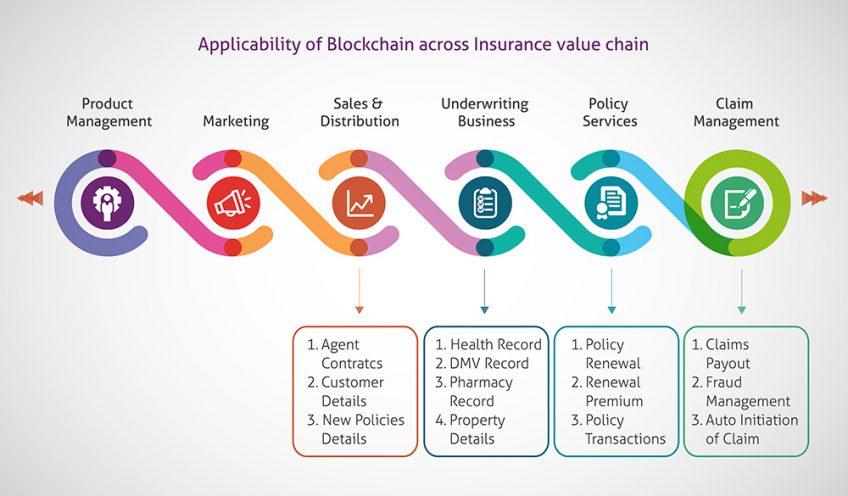

The main areas that blockchain technology is likely to improve are as follows:

1. Improving trust

We face a crisis of trust in the financial sector today. Although the primary focus is on large banks, a lack of trust is going to have a negative impact on all associated sectors, including insurance. Inefficiencies and high costs, coupled with a lack of confidence, have led to more and more people failing to take out insurance.

Take the average California household, for instance. Only 17% of the total population of the state is insured for earthquake insurance, despite there being a high risk of earthquakes and related losses. With the transparency offered by Blockchain technology, the trust factor can be regained between the parties involved.

2. Enhancing efficiency

If you have ever tried to change your healthcare provider or insurance company, you would know the vast amount of paperwork that you are required to deal with. Also, this method of data storage is widely inefficient. Added to this, people are often reluctant to share data, fearing a loss or theft of personal data.

Implementing blockchain technology would create added security and efficiency in data handling procedures. Since data cannot be altered once written, it can be trusted as being completely accurate.

3. Improving the procedures of claim processing

The insurance claims process itself is very drawn-out. It involves many separate stages that must be completed in order to fulfill a claim. Many of the underlying advantages of blockchain, including smart contracts, will help to streamline these processes.

Let‘s look at how this will happen.

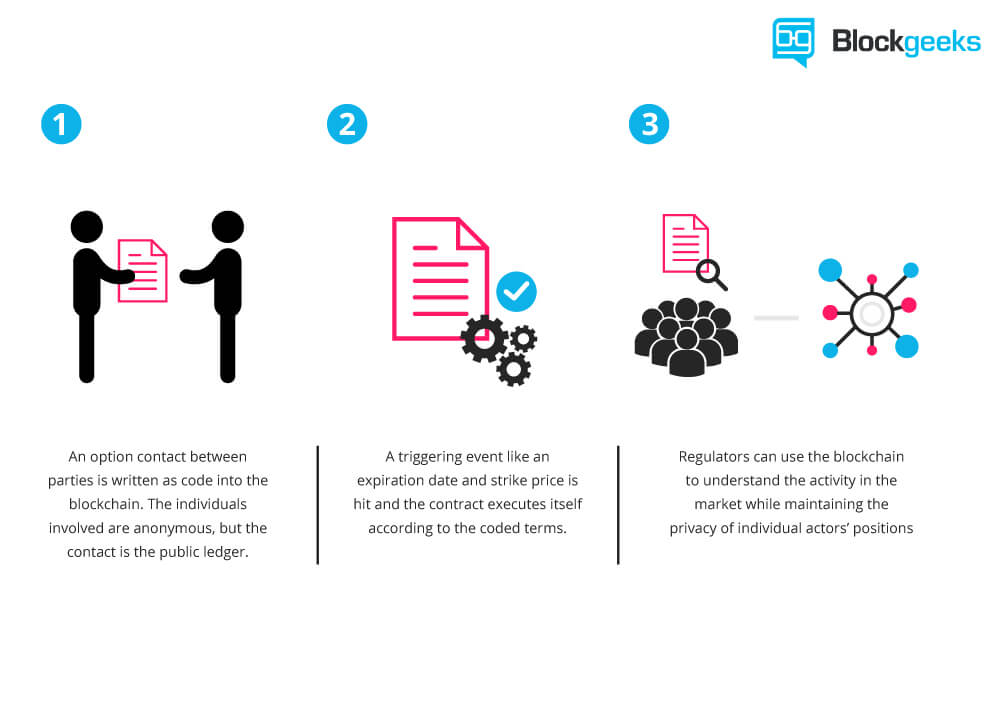

4. Smart Contracts

Everything from creating new insurance contracts to notifying police of fraudulent claims can be handled by smart contracts.

A smart contract can be programmed to enact a whole range of actions based on certain criteria being fulfilled. One such example would be in reporting fraud.

If a person initiated a claim for a stolen TV, for example, a claim would automatically start. During this process, if one or more predetermined conditions to identify suspicious behavior were detected, such as a past history of fraud or an identical past claim.

For example, the smart contract would automatically initiate a deeper investigation or report the information of suspected fraud accounts to the police.

A smart contract helps automate claims processing and claim payments, and close claims as it has oversight of the entire insurance process.

5. Detecting and Preventing Fraud

According to the statistics collected by the Coalition Against Insurance Fraud, insurance fraud costs about $80 billion a year. Not only does this bump up insurance premiums, but it also increases processing times and the amount of industry oversight that is required.

1,200 top developers

us since 2016

This is one of the most compelling reasons for the incorporation of Blockchain in insurance.

Blockchain Use Cases for the Insurance Industry

Some of the blockchain insurance use cases are as follows:

1. Client onboarding

In order to satisfy the requirements of Know Your Customer (KYC), insurance providers are required to collect, verify, and validate a number of key documents that help to prove identification.

Each one of these documents needs to be reviewed by internal departments to complete the processes. This means time, money, and longer processing times. Companies will also have to spend even more resources to fix any errors that might have occurred during the process.

Since a blockchain network is distributed, it is possible to make all the necessary documentation available to anyone with permission to access the network.

Records cannot be altered retroactively, making them 100% trustworthy. This helps to facilitate the secure sharing of data and information to approved third parties and across the organisation.

There is no way they could alter the data unless they happen to have a quantum computer that has not even been invented yet.

Securing customer identities on blockchain has other benefits as well. The most important thing is that people will easily be able to verify their identity without the need to go to other parties to double-check.

2. Underwriting

The process of underwriting involves the evaluation of various parameters, including the risk associated with furnishing a policy for a client, the calculation of the coverage that a client is liable to receive, and the premium that should be paid by the client for the coverage.

Insurance is often said to be a gamble. However, no good insurance company will take chances without knowing its data is correct. Accessing the real risk that a person or company poses is a huge challenge. In some cases, this can be a lengthy procedure, which requires many people to undertake an evaluation of the full scope of risk vs. reward.

With blockchain solutions, risk liability can be decreased, and semi-automatic pricing models can be refined in real-time. If the system detects a large number of smart contract-based policies being paid out for one particular risk, e.g., car theft within the same area, it can adjust the price of new policies in that area.

This fact will help shorten and automate the underwriting process, effectively reducing operational costs.

IBM, Standard Chartered, and AIG have already successfully piloted smart contracts on a dedicated blockchain. While it is still early days, the fact that such powerhouses of industry are already exploring blockchain is a sign of the enormous potential it has to offer.

Blockchain Insurance App Development

Blockchain brings with it bountiful opportunities for the insurance industry. With its underlying attributes such as smart contracts, proof of concept, distributed ledger technology, and non-repudiation capabilities, it can also be used to create insurance apps.

These apps could be one of the most game-changing applications of blockchain technology. As part of an IoT network, a blockchain insurance app could offer the first-ever pay-as-you-go insurance plans.

Such plans would allow people to only pay for insurance when they need it. So, in the example of car insurance, accident insurance would only be activated when the car was being used. The rest of the time, a fire and theft policy could cover the vehicle.

Not only would this save money, but factors such as driving style could help target higher-risk people and charge them accordingly.

The Future: An Insurance Industry Powered by Blockchain

As I have highlighted, there are a number of advantages that blockchain has over existing solutions. Giant players in the insurance sector, such as Swiss Re and Allianz, are already in the process of developing blockchain-based solutions.

However, transforming the whole insurance sector with blockchain technology is no easy task. Realistically, it requires a great deal of effort for the companies to align around the processes and standards within the technology before it can even be implemented.

Along with this, governments will need to design and issue new insurance policies and guidelines on how the technology can be used. Just think of the potential errors a more automated system could create, and the policyholder themselves would have to be satisfied with the change, too.

Despite this, it seems certain that the insurance industry is going to be one of the major beneficiaries of blockchain-based solutions.

If you are planning to invest in blockchain technology for your business, DevTeam.Space can help you. We have a team of high-quality blockchain developers experienced in developing market-competitive software solutions using cutting-edge technologies.

You can share with us your initial details for a blockchain development project via this quick form, and one of our technical managers will get back to you to assist you further with project planning and to connect you with the right software engineers.

Frequently Asked Questions on Blockchain for the Insurance Industry

The main area where Bitcoin will benefit insurance processes is in improving automation. Smart contracts will allow for the automation of many processes, including claims processing, as well as prevent insurance fraud.

Automation and the reduction of successful fraudulent claims stand to benefit the blockchain-powered insurance industry hundreds of millions of dollars a year. Blockchain will facilitate much of the automation the industry undertakes over the next few decades.

Every single major industry stands to benefit from blockchain. However, it is the financial industry, healthcare, and the insurance industry that stand to benefit the most.

Alexey Semeney

Founder of DevTeam.Space

Hire Alexey and His Team To Build a Great Product

Alexey is the founder of DevTeam.Space. He is award nominee among TOP 26 mentors of FI's 'Global Startup Mentor Awards'.

Alexey is Expert Startup Review Panel member and advices the oldest angel investment group in Silicon Valley on products investment deals.